According to our analysis natural gas moved 34 ticks on DOE Natural Gas Storage Report data on 24 October 2024.

Natural gas (38 ticks)

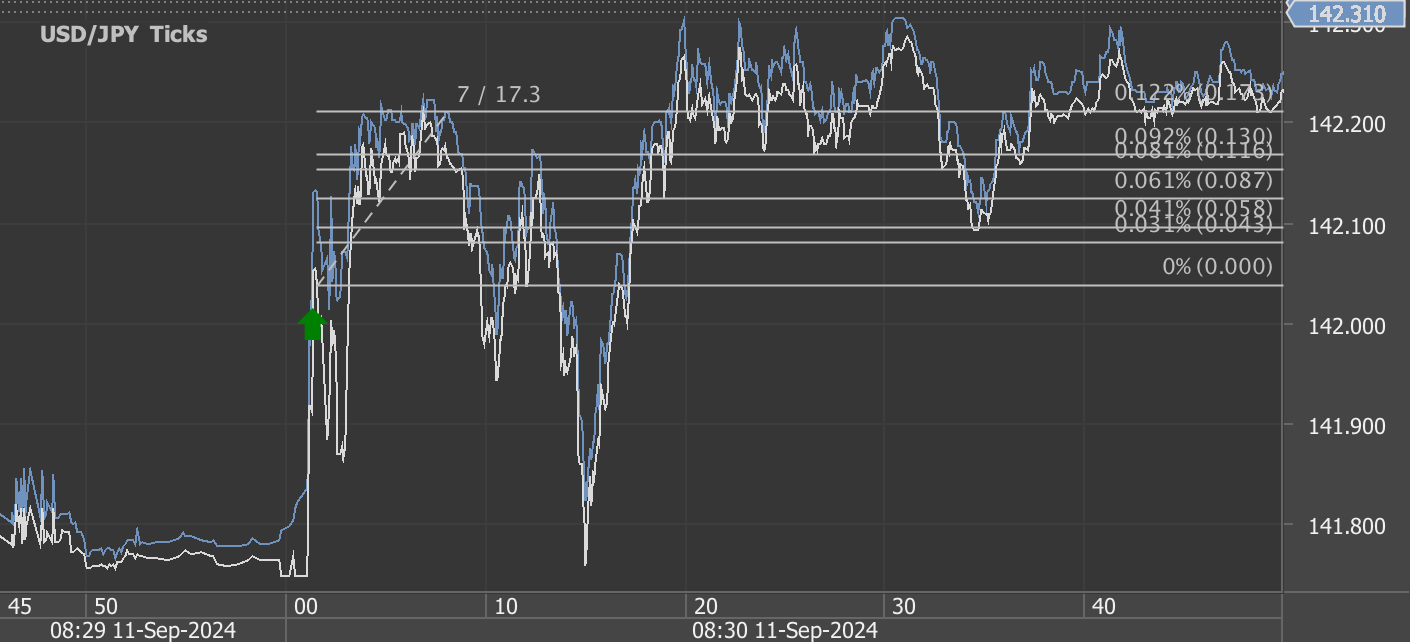

Charts are exported from JForex (Dukascopy).

Weekly Natural Gas Storage Report: October 18, 2024 – Key Highlights and Insights

As we approach the colder months, the latest Weekly Natural Gas Storage Report released by the U.S. Energy Information Administration (EIA) offers crucial insights into the current state of natural gas reserves. For the week ending October 18, 2024, working gas in underground storage across the Lower 48 states reached 3,785 billion cubic feet (Bcf), representing a net increase of 80 Bcf compared to the previous week. This puts total storage levels 106 Bcf higher than the same period last year and 167 Bcf above the five-year average.

Regional Breakdown and Implied Flows

The report highlights steady growth in gas reserves across various regions:

East Region: The working gas in storage increased by 8 Bcf to reach 901 Bcf, which is slightly below last year’s figure of 905 Bcf, representing a small 0.4% decrease. However, it remains 1.9% above the five-year average of 884 Bcf.

Midwest Region: A significant uptick of 21 Bcf brought storage to 1,088 Bcf. This represents a 1.9% increase from last year and a 3.0% increase over the five-year average of 1,056 Bcf, signaling healthy storage levels in this critical region.

Mountain Region: Although the region saw a smaller increase of 4 Bcf, its reserves now stand at 291 Bcf, marking a substantial 15.9% growth compared to last year and a 30.5% rise over the five-year average, which sits at 223 Bcf. This is one of the most pronounced increases of all regions.

Pacific Region: With an additional 7 Bcf, the Pacific region’s gas reserves are now at 300 Bcf. This is 6.4% higher than last year’s 282 Bcf and 6.8% above the five-year average of 281 Bcf.

South Central Region: The largest weekly net change came from the South Central region, where storage levels increased by 39 Bcf, reaching a total of 1,205 Bcf. This includes a 21 Bcf increase in salt-dome storage, now at 314 Bcf, and a 19 Bcf increase in nonsalt storage, bringing that total to 891 Bcf. The region is performing 2.7% better than last year and is 2.6% above the five-year average.

Total Storage and Implications

At 3,785 Bcf, total working gas in storage is comfortably within the five-year historical range. This storage level provides a cushion as we head into the winter heating season, where demand typically spikes. The net increase of 80 Bcf from the prior week is a healthy signal that the market is preparing adequately for potential weather-driven demand surges in the coming months.

The 106 Bcf year-over-year surplus and 167 Bcf surplus over the five-year average indicate robust storage levels, which should help moderate price volatility as temperatures drop and heating demand rises. With winter approaching, natural gas storage figures will be critical in determining price stability and supply adequacy in the coming months.

Key Takeaways:

Healthy Storage Levels: The 3,785 Bcf in storage positions the market well for the winter season, with a notable 106 Bcf increase over last year.

Regional Variations: Some regions, like the Mountain and Pacific, are showing significant year-over-year increases, reflecting improved storage capabilities and preparedness.

Implied Flow of 80 Bcf: The overall weekly increase of 80 Bcf is consistent with seasonal storage trends and ensures a stable supply going into winter.

Price and Supply Outlook: With storage levels above historical averages, there’s a strong foundation to mitigate supply concerns and manage price spikes that may arise from unexpected weather events or surges in demand.

The next release on October 31, 2024, will offer further insight as we monitor natural gas reserves closely during this critical period. Stay tuned for updates, as storage dynamics play a crucial role in the natural gas market and energy planning throughout the winter season.

Source: https://ir.eia.gov/ngs/ngs.html

Start futures forex fx commodity news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.