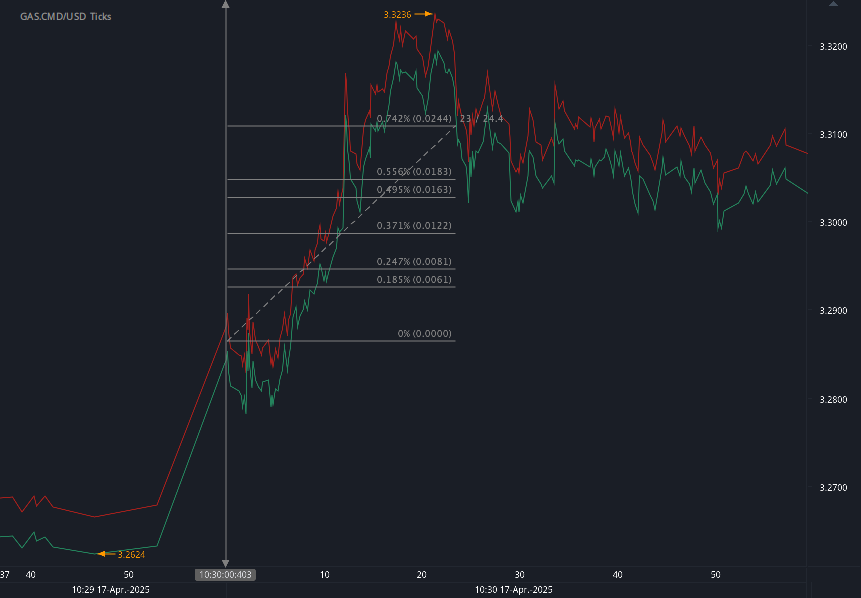

According to our analysis crude oil moved 19 ticks on DOE Petroleum Status Report data on 23 April 2025.

Light sweet crude oil (19 ticks)

Charts are exported from JForex (Dukascopy).

U.S. Weekly Petroleum Snapshot – April 18, 2025

The U.S. petroleum landscape for the week ending April 18, 2025, reveals a dynamic balance of supply, demand, and prices amid seasonal transitions and evolving energy trends. Let’s break down the latest Weekly Petroleum Status Report from the U.S. Energy Information Administration (EIA).

Refinery Operations and Output

U.S. crude oil refinery inputs averaged 15.9 million barrels per day, rising by 326,000 barrels per day compared to the previous week. Refineries operated at 88.1% of their operable capacity, reflecting an uptick as refineries ramp up ahead of peak driving season.

Gasoline production: Rose to 10.1 million barrels/day

Distillate fuel production: Dropped slightly to 4.6 million barrels/day

Imports and Inventories

Crude oil imports fell notably:

Crude imports: Dropped to 5.6 million barrels/day, down 412,000 from the previous week

Four-week average: 6.1 million barrels/day, 6.8% lower than last year

Meanwhile, inventory trends showed a mixed bag:

Crude oil inventories (excluding SPR): Up by 0.2 million barrels to 443.1 million barrels, still 5% below the five-year seasonal average

Gasoline inventories: Down 4.5 million barrels, now 3% below average

Distillate inventories: Down 2.4 million barrels, a significant 13% below average

Propane/propylene: Up 2.3 million barrels, but 7% below average

Total commercial petroleum inventories: Declined 0.7 million barrels

Product Demand

Demand remained relatively strong:

Total products supplied: Averaged 19.9 million barrels/day, up 0.4% year-over-year

Gasoline supplied: 8.7 million barrels/day, slightly down (0.4%) from last year

Distillate fuel supplied: 3.9 million barrels/day, up a robust 12.8%

Jet fuel supplied: Surged 13.8%, signaling increased air travel demand

Retail Fuel Prices

Prices continued their downward trend:

Regular gasoline: Averaged $3.141/gallon, down $0.027 from last week and $0.527 below last year

Diesel fuel: Averaged $3.534/gallon, down $0.045 week-over-week and $0.458 below year-ago levels

Looking Ahead

The report suggests a seasonal tightening in gasoline inventories even as production ramps up. Meanwhile, strong distillate and jet fuel demand reflects broader economic activity. Retail fuel prices remain considerably lower than in 2024, which could support continued consumer travel and freight movement into the summer.

Refiners appear to be preparing for peak season with increased utilization and production. However, below-average inventories in key product categories may make markets more sensitive to disruptions or spikes in demand.

Conclusion With gasoline inventories dropping and demand for jet and distillate fuels rising sharply, all eyes are on how refiners and importers respond heading into summer. Continued lower prices at the pump are welcome news for consumers, though tightening supply conditions warrant close monitoring.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Source: https://www.eia.gov/petroleum/supply/weekly/archive/2025/2025_04_23/pdf/highlights.pdf

Start futures forex fx commodity news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.