We are pleased to announce that there was a potential of 876 pips/ticks profit out of the following 13 events in the third quarter of 2024 based on our ex-post analysis. The potential performance for 2023 was 13,607 pips/ticks.

Q3 2024

US BLS Consumer Price Index (CPI) (32 pips / 11 July 2024)

Sweden Consumer Price Index (CPI) (272 pips / 12 July 2024)

USDA WASDE (World Agricultural Supply and Demand Estimates) (40 ticks / 12 July 2024)

US Retail Sales (40 pips / 16 July 2024)

DOE Natural Gas Storage Report (32 ticks / 18 July 2024)

DOE Natural Gas Storage Report (40 ticks / 25 July 2024)

US Employment Situation (Non-farm payrolls / NFP) (90 pips / 2 August 2024)

US Retail Sales (84 pips / 15 August 2024)

DOE Natural Gas Storage Report (38 ticks / 15 August 2024)

US Gross Domestic Product (GDP) (47 pips / 29 August 2024)

US BLS Job Openings and Labor Turnover Survey (JOLT) (72 pips / 4 September 2024)

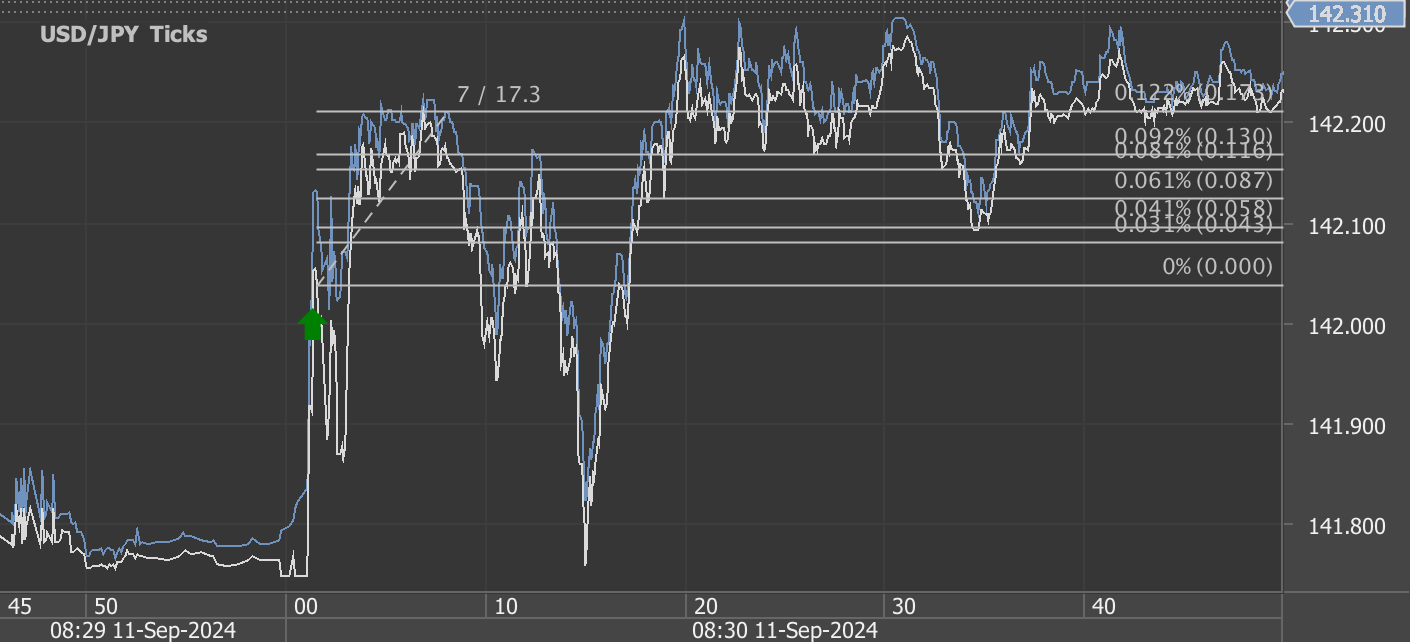

US BLS Consumer Price Index (CPI) (27 pips / 11 September 2024)

FOMC Interest Rate Decision and Projections (62 pips / 18 September 2024)

Total trading time would have been around 12 minutes in 3 months! (preparation time not included)

Q3 2024 Economic Review: Key Trends and Market Insights

As we close out the third quarter of 2024, it's clear that this period has been defined by significant economic shifts, market volatility, and pivotal policy decisions. Traders and investors in forex, equity and commodities markets have witnessed sharp market movements, particularly in response to macroeconomic data releases, monetary policy decisions, and inflationary pressures. The potential trading profit from machine-readable data feeds like Haawks G4A was substantial, with multiple high-impact events driving opportunities across global markets.

Let’s take a look back at the key trends, events, and economic insights from Q3 2024.

Labor Market Resilience and Inflation Stubbornness

Q3 began with continued strength in the U.S. labor market, marked by steady job openings and persistent wage growth, despite efforts by the Federal Reserve to cool down inflation. Reports like the U.S. Job Openings and Labor Turnover Survey (JOLTS) in both August and September revealed a tight labor market, with job openings climbing above 8 million.

The resilience of the labor market presented a dilemma for policymakers: while robust employment is a positive economic indicator, it also contributes to inflationary pressures. Higher wages, combined with strong consumer demand, added to the sticky inflation landscape that the Federal Reserve has been trying to manage since 2022.

Despite the Fed’s aggressive tightening cycle, inflation remained higher than the desired 2% target, especially when looking at core inflation metrics. Energy prices, particularly gasoline, surged again in September, further fueling price increases. The Consumer Price Index (CPI) reports for July, August, and September all pointed to ongoing inflation, with price increases driven by energy, housing, and services.

Key Events Driving Market Movements

Several economic releases and policy announcements drove sharp market movements throughout Q3, providing traders with ample opportunities for potential profits using Haawks G4A machine-readable data feeds. Here are some of the most significant:

1. US Non-Farm Payrolls (NFP) – August 2, 2024

The Non-Farm Payrolls (NFP) report kicked off Q3 with a notable surprise: weaker-than-expected job growth. This led to a 90-pip market movement, as traders speculated that the Federal Reserve might slow down its monetary tightening due to the possibility of an economic slowdown. The weaker NFP numbers were one of the first signs that the U.S. labor market might be losing steam, signaling potential softening ahead.

2. FOMC Rate Cut – September 18, 2024

One of the most important events in Q3 was the Federal Open Market Committee (FOMC) decision to cut interest rates by 50 basis points in September. This marked the first rate cut since 2022, lowering the federal funds rate to a range of 4.75% - 5.00%. The rate cut was a response to softer economic data and inflation that, while moderating, still posed risks to the broader economy.

This move triggered a significant 62-pip reaction in the markets, as investors recalibrated expectations for the future path of Fed policy. Traders quickly adjusted their positions, anticipating further cuts in the coming months as the Fed aims to balance economic growth with price stability.

3. U.S. Consumer Price Index (CPI) – Monthly Reports

Inflation data remained a focal point for traders throughout Q3, with CPI reports showing inflation still above target. While headline inflation showed some moderation, core inflation, which excludes volatile food and energy prices, remained sticky. The July CPI report saw a 32-pip movement, while the August and September reports led to additional fluctuations in the markets, as traders adjusted their expectations for future Fed rate cuts or potential reversals.

Global Economic Developments

While the U.S. economy was the dominant focus of Q3, global developments also played a role in shaping the economic landscape. Sweden, for instance, saw its Consumer Price Index (CPI) rise sharply in July, triggering a 272-pip market movement. This significant jump suggested that inflationary pressures were also present in Europe, prompting central banks, like Sweden’s Riksbank, to adopt a more hawkish stance to curb rising prices.

Commodity markets also saw significant action during the quarter. The Department of Energy's (DOE) Natural Gas Storage Reports, released in July and August, resulted in substantial movements in natural gas prices as supply-demand dynamics continued to affect energy costs worldwide. This volatility provided further opportunities for traders involved in energy commodities.

The Federal Reserve's Balancing Act

Perhaps the defining feature of Q3 2024 was the Federal Reserve’s cautious shift in policy. After a prolonged period of aggressive rate hikes to combat inflation, the Fed’s decision to cut rates in September signaled a more measured approach. However, the central bank made it clear that future rate cuts would depend on incoming data, particularly inflation and labor market trends.

As we look ahead to Q4, market participants will closely monitor the evolving economic landscape, especially as the Fed navigates the delicate balance between supporting economic growth and achieving price stability.

What Lies Ahead in Q4 2024?

The fourth quarter of 2024 is set to bring more significant economic events, with traders and investors likely to focus on several key indicators:

Further Labor Market Data: Will job growth continue to slow, and will wage pressures ease enough to allow inflation to come down?

Inflation Reports: As energy prices fluctuate, traders will be keen to see whether inflation moderates in Q4, influencing future Fed rate decisions.

Global Economic Health: With other central banks also grappling with inflation, global economic trends will play a crucial role in shaping market movements.

For traders leveraging Haawks G4A low-latency data feeds, staying informed and reacting quickly to these developments will be key to maximizing potential profits as markets continue to experience volatility.

Conclusion

Q3 2024 was a dynamic and eventful period, marked by resilient labor markets, persistent inflation, and a notable shift in U.S. monetary policy. Traders who utilized machine-readable data to respond quickly to these economic releases were well-positioned to capitalize on significant market movements. As we head into the final quarter of the year, the economic landscape remains uncertain, but opportunities for informed and strategic trading abound.

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Start futures/forex/oil/grains news trading with Haawks G4A low latency machine-readable data today, we offer one of the fastest machine-readable data feeds for US macro-economic and commodity data and macro-economic data from Norway, Sweden, Switzerland Turkey and ECB interest rates and statement.

Please let us know your feedback and check out our G4A low latency data feed.

All data is machine readable and available via API access in Aurora, CH1, NY4 and LD4. Free trials.