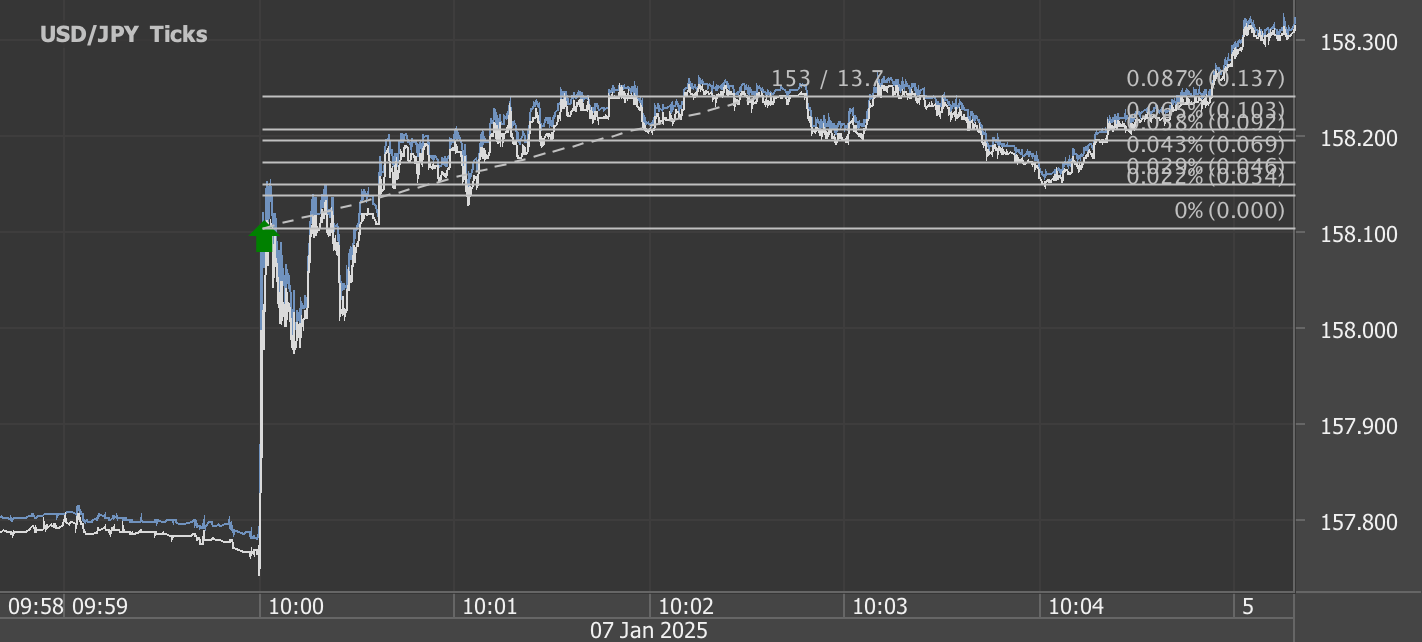

According to our analysis USDJPY and EURUSD moved 15 pips and US30 moved 26 points on US BLS Job Openings and Labor Turnover Survey (JOLT) data on 4 February 2025.

USDJPY (9 pips)

EURUSD (6 pips)

US30 (26 points)

Charts are exported from JForex (Dukascopy).

Job Openings and Labor Turnover: What Traders Need to Know

The latest Job Openings and Labor Turnover Survey (JOLTS) report from the Bureau of Labor Statistics (BLS) offers key insights into the U.S. labor market for December 2024. With job openings declining, hiring slowing, and layoffs rising in certain sectors, traders should closely analyze these trends to anticipate market movements.

Key Takeaways for Traders

1. Job Openings Drop to 7.6 Million

December saw a decrease of 556,000 job openings, bringing the total to 7.6 million.

This marks a 1.3 million decline over the year, indicating a cooling labor market.

Sectors Hit Hardest:

Professional and business services (-225,000)

Healthcare and social assistance (-180,000)

Finance and insurance (-136,000)

Sector Showing Growth:

Arts, entertainment, and recreation (+65,000)

Trader Insight: A declining job openings rate (now at 4.5%) suggests economic slowdown, which could weigh on consumer spending and corporate earnings.

2. Hiring Activity Remains Weak

The number of hires in December remained flat at 5.5 million, down 325,000 year-over-year.

Hiring in finance and insurance increased by 48,000, which may indicate resilience in this sector.

Trader Insight: Weak hiring points to softening corporate growth and potential downward pressure on equities, particularly in sectors with job losses.

3. Separations: Layoffs vs. Quits

Total separations (quits, layoffs, discharges) held steady at 5.3 million.

Quits Rate:

2.0% (unchanged)

Total quits fell by 242,000 YoY, showing reduced worker confidence.

Quits declined in transportation, warehousing, and utilities (-42,000), suggesting slowing activity in logistics.

Layoffs & Discharges:

Increased in transportation, warehousing, and utilities (+87,000).

Increased in mining and logging (+6,000).

Trader Insight: Rising layoffs in transportation and warehousing could signal slowing global trade, negatively impacting companies in shipping, logistics, and e-commerce.

Market Implications

Equities:

Bearish: Sectors seeing major job losses (finance, healthcare, business services) may face weaker earnings.

Bullish: Companies in entertainment and recreation show hiring growth, suggesting some resilience in consumer discretionary spending.

Fixed Income:

A softening labor market could lead to increased Federal Reserve dovishness, supporting lower bond yields and a rally in Treasuries.

FX Markets:

Dollar Weakness? A weakening job market might prompt a less aggressive Fed, potentially denting USD strength.

Safe Haven Flows: If economic slowdown fears grow, expect flows into JPY and CHF.

Commodities:

Oil Impact: Increased layoffs in transportation and logistics suggest potential demand weakness, which could weigh on crude prices.

Gold Strength: Rising economic uncertainty may drive safe-haven demand for gold.

Looking Ahead: January 2025 Report

The next JOLTS report (January 2025) will be released on March 11, 2025. Traders should monitor labor market trends alongside inflation data, GDP growth, and Fed policy shifts for a broader market outlook.

Bottom Line: A cooling labor market is a warning signal for traders. Weaker hiring, falling job openings, and increasing layoffs point to slower economic growth—a potential headwind for risk assets. Stay ahead by adjusting strategies accordingly!

Disclaimer: This blog post is for informational purposes only and should not be construed as financial advice. Always conduct thorough research and consider seeking advice from a financial professional before making any investment decisions.

Start futures #forex fx news #trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.