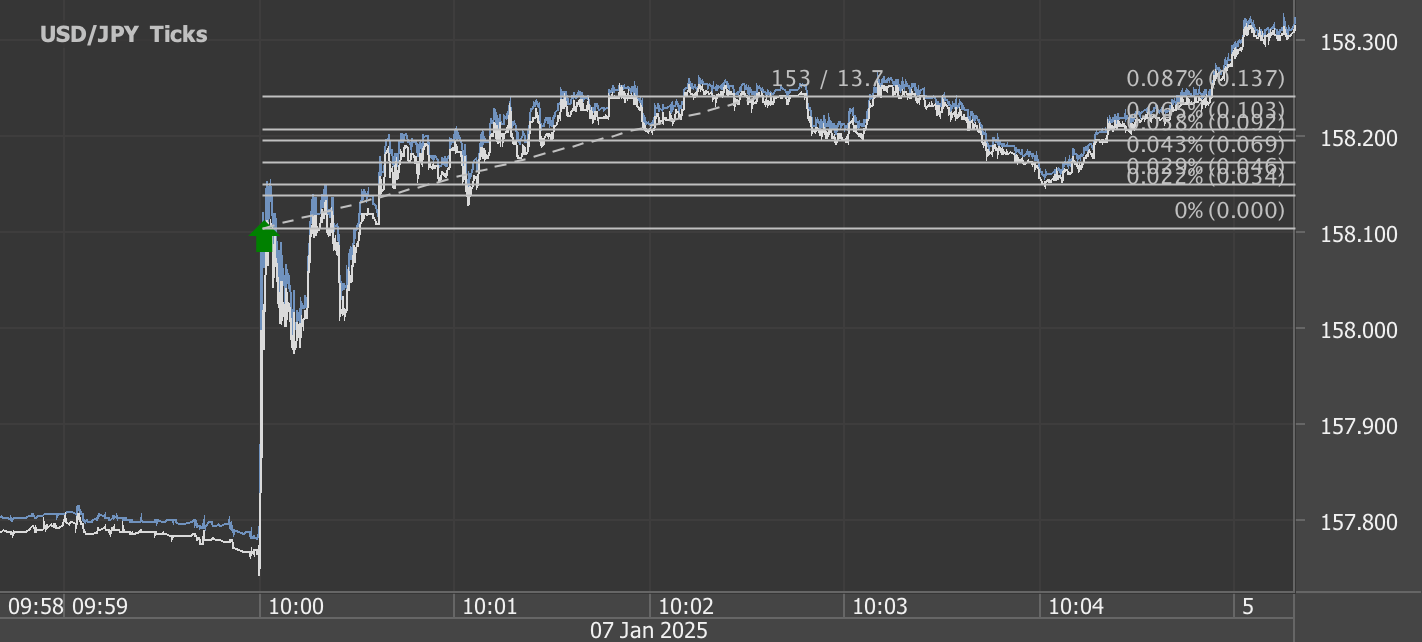

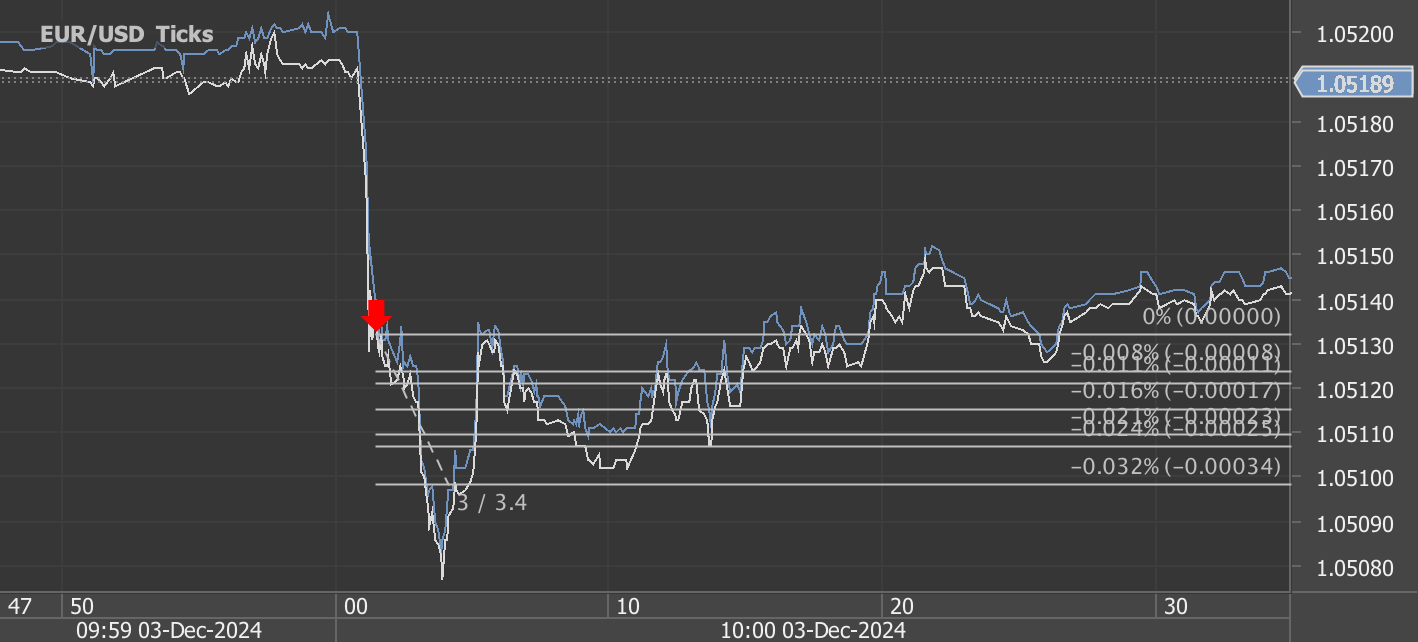

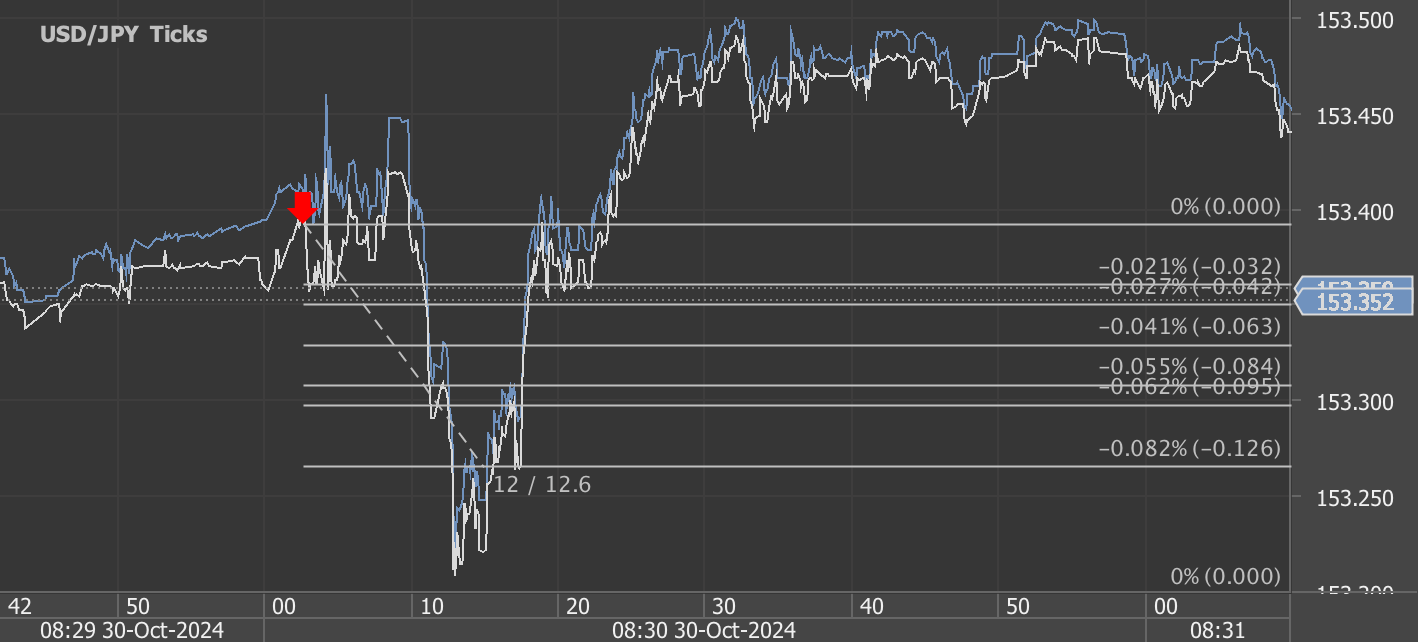

According to our analysis USDJPY, EURUSD and US30 moved around 35 pips and 210 points on US Employment Situation (Non-farm payrolls / NFP) data on 10 January 2025.

USDJPY (19 pips)

EURUSD (16 pips)

US30 (210 points)

Charts are exported from JForex (Dukascopy).

December 2024 Employment Report: Key Takeaways for Traders

The U.S. Bureau of Labor Statistics (BLS) released its December 2024 Employment Situation Report today, revealing a mixed but largely positive labor market. Here’s what traders need to know and how the data could influence markets in the near term.

Key Highlights of the Report

Nonfarm Payroll Growth:

Nonfarm payrolls increased by 256,000, beating market expectations. Gains were led by health care, government, social assistance, and retail trade.Unemployment Rate:

The unemployment rate held steady at 4.1%, indicating a resilient labor market despite concerns of potential softening.Wage Growth:

Average hourly earnings increased by 0.3% month-over-month (+10 cents), bringing the annual wage growth to 3.9% year-over-year.Labor Force Participation Rate:

Unchanged at 62.5%, maintaining the same range seen throughout 2024.

Market Implications

1. Equity Markets:

Bullish Signal: The robust payroll growth could support cyclical sectors like retail, health care, and consumer discretionary.

Earnings Potential: With strong wage gains and improved retail hiring, markets may see positive sentiment heading into Q1 earnings season.

Caveat: If wage growth accelerates beyond expectations in future reports, it could reignite inflation fears.

2. Bond Markets:

The steady unemployment rate and solid job gains could increase the likelihood of the Federal Reserve holding interest rates steady. However, continued strength may push yields higher if investors price in a more hawkish Fed stance.

3. Forex Market:

The U.S. dollar may strengthen in response to better-than-expected job numbers, as it reinforces confidence in the U.S. economy.

Watch for USD pairs, particularly with currencies of economies that are experiencing slower labor market recoveries.

Sector Breakdown for December 2024

Health Care (+46,000 jobs): Gains were seen across home health care services (+15,000), nursing care facilities (+14,000), and hospitals (+12,000). This continued sector strength may benefit health care ETFs and equities.

Retail Trade (+43,000 jobs): A recovery from November’s losses was driven by increases in apparel, general merchandise, and health and personal care stores. Retail-focused traders may view this as a sign of resilient consumer demand.

Government (+33,000 jobs): Job gains, primarily in state government roles, continued a positive trend, though at a slower pace than in 2023.

Social Assistance (+23,000 jobs): Continued steady growth here supports the broader theme of demand for care services.

Wage and Workweek Trends

Average Hourly Earnings: Up $0.10 to $35.69 (+3.9% YoY).

Production and Nonsupervisory Workers: Wages increased by $0.06 to $30.62, signaling continued earnings momentum for middle-income workers.

However, the average workweek remained at 34.3 hours, unchanged for the fifth consecutive month, indicating stable labor utilization across sectors.

Revisions and Seasonal Adjustments

The revisions for October and November combined resulted in a net downward adjustment of 8,000 jobs. Traders should take note of these recalibrations, which may indicate some volatility in reporting but largely point to a stable employment trend.

Key Risks to Watch

Fed Policy: Traders should monitor any commentary from Federal Reserve officials, as this report keeps the door open for either policy stability or future tightening if wage pressures persist.

Economic Slowdown Concerns: While the labor market remains strong, longer-term concerns about a potential slowdown in consumer spending or corporate hiring could affect future payroll reports.

Global Market Sentiment: The forex and commodity markets could be impacted by how global investors interpret the U.S. labor market’s strength relative to international economic conditions.

Conclusion

The December 2024 employment report reinforces the narrative of a robust U.S. labor market with healthy job creation, stable unemployment, and moderate wage growth. Traders should position themselves for potential equity market gains in cyclical sectors while keeping a close eye on bond yields and the Federal Reserve's evolving stance. The next employment report, scheduled for February 7, 2025, will provide further clues as to whether this momentum can continue into the new year.

Start forex fx futures news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.