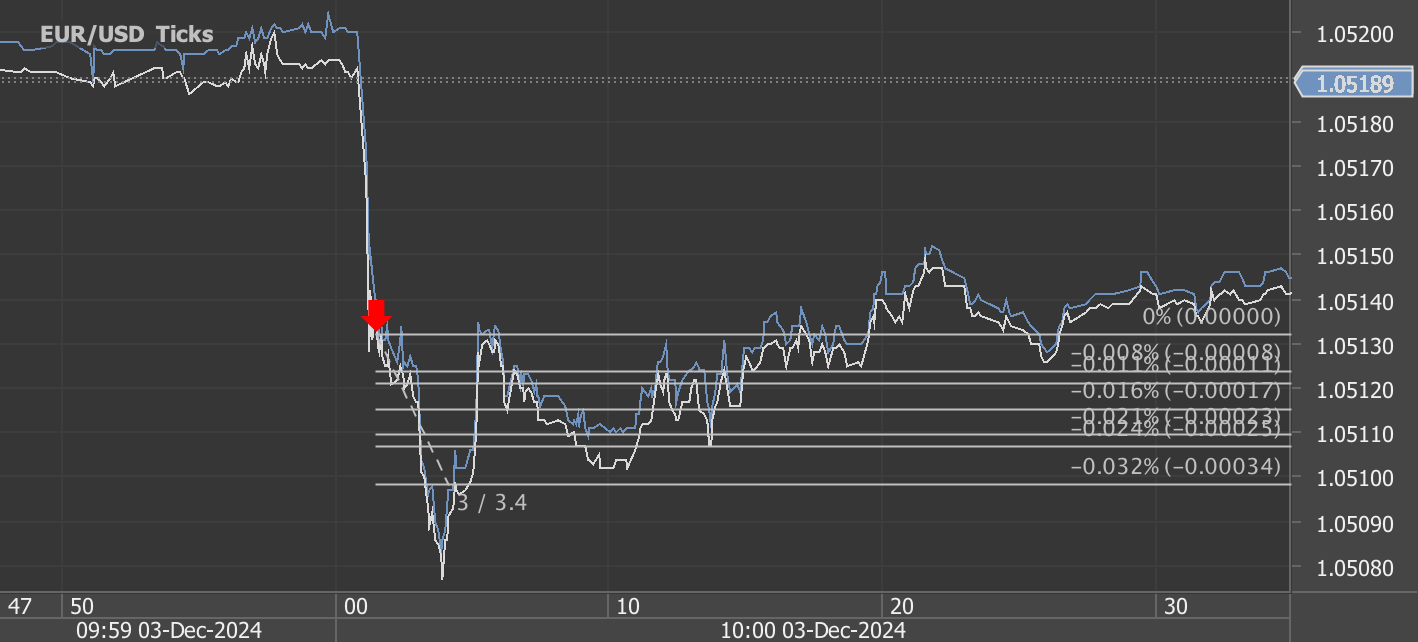

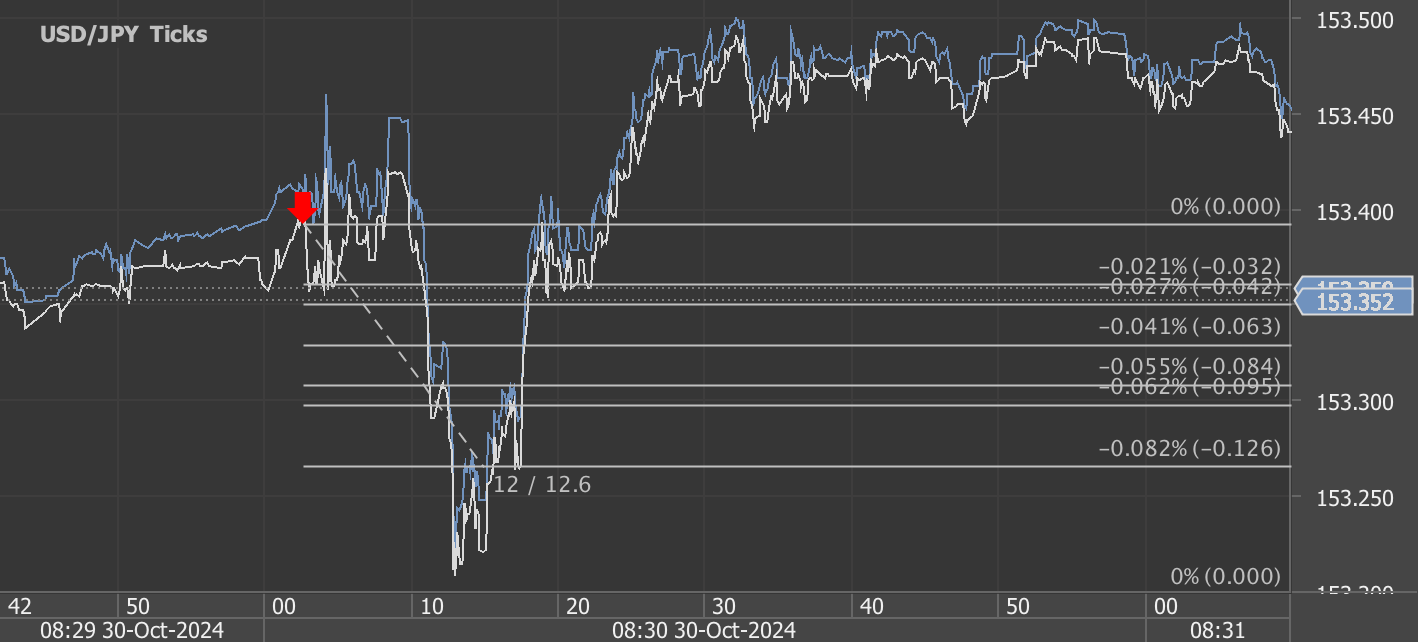

According to our analysis USDJPY and EURUSD moved around 37 pips on US Employment Situation (Non-farm payrolls / NFP) data on 6 December 2024.

USDJPY (28 pips)

EURUSD (9 pips)

Charts are exported from JForex (Dukascopy).

November 2024 U.S. Employment Report: Key Takeaways and Insights

The U.S. Bureau of Labor Statistics (BLS) released its November 2024 Employment Situation Report, highlighting continued growth in the labor market with some mixed signals. Here’s what you need to know:

Job Growth Surges, Led by Health Care and Leisure Industries

Nonfarm payroll employment increased by 227,000 in November, marking a strong rebound from the previous month's modest gain of 36,000. This growth surpasses the 12-month average increase of 186,000, signaling resilience despite broader economic uncertainties. Key contributors included:

Health Care (+54,000): Growth was driven by ambulatory health care services (+22,000), home health care (+16,000), hospitals (+19,000), and nursing care facilities (+12,000).

Leisure and Hospitality (+53,000): Food services and drinking places added the bulk of these jobs (+29,000), reflecting ongoing recovery in service-related industries.

Government (+33,000): Gains were concentrated in state government employment (+20,000).

Transportation Equipment Manufacturing (+32,000): The return of workers following strike actions fueled this sector’s rebound.

Unemployment Rate Holds Steady, but Challenges Persist

The unemployment rate remained relatively stable at 4.2%, up from 3.7% a year earlier. There are now 7.1 million unemployed Americans, reflecting ongoing challenges in the labor market recovery. Notable trends include:

Long-term Unemployment: This group, defined as those jobless for 27 weeks or more, remains elevated at 1.7 million, making up 23.2% of total unemployed.

Demographic Insights: Unemployment edged up for Black workers to 6.4%, while other major groups, including Whites (3.8%), Asians (3.8%), and Hispanics (5.3%), showed little change.

Labor Force and Participation Trends

The labor force participation rate was unchanged at 62.5%, maintaining a narrow range since late 2023. However, the employment-population ratio declined by 0.6 percentage points over the past year, landing at 59.8%. These metrics suggest some stagnation in workforce engagement.

Retail Trade Slumps as Seasonal Hiring Falters

Retail trade lost 28,000 jobs in November, marking a significant divergence from other industries. Losses were particularly sharp in general merchandise retailers (-15,000), though electronics and appliance retailers posted modest gains (+4,000). This decline could reflect shifting consumer patterns and cautious hiring ahead of the holiday season.

Earnings and Work Hours Tick Up

Wage growth continued at a steady pace, with average hourly earnings increasing by 0.4% to $35.61. Over the past year, wages have risen by 4.0%, providing some relief against inflationary pressures. The average workweek for private nonfarm employees edged up to 34.3 hours, a positive indicator of labor demand.

Upward Revisions Reflect Stronger Momentum

Revised data for September and October show that employment gains were 56,000 higher than previously reported. September’s total was adjusted up to 255,000, and October’s figure increased to 36,000.

What It All Means

November’s employment report paints a picture of a labor market balancing growth with persistent challenges:

Encouraging Sectors: Health care, leisure, and government sectors are driving job creation, reflecting the continued demand for essential services.

Emerging Concerns: Retail trade losses and elevated long-term unemployment suggest pockets of weakness that merit attention.

Stable Wages: The steady rise in wages is a positive for workers, though it remains to be seen if this can keep pace with inflation and higher living costs.

As we close out 2024, the labor market appears robust but not without its vulnerabilities. Policymakers, businesses, and job seekers will be closely watching December’s report, due on January 10, 2025, to gauge the economy’s trajectory into the new year.

Stay tuned for more updates on labor market trends and insights!

Start forex fx futures news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.