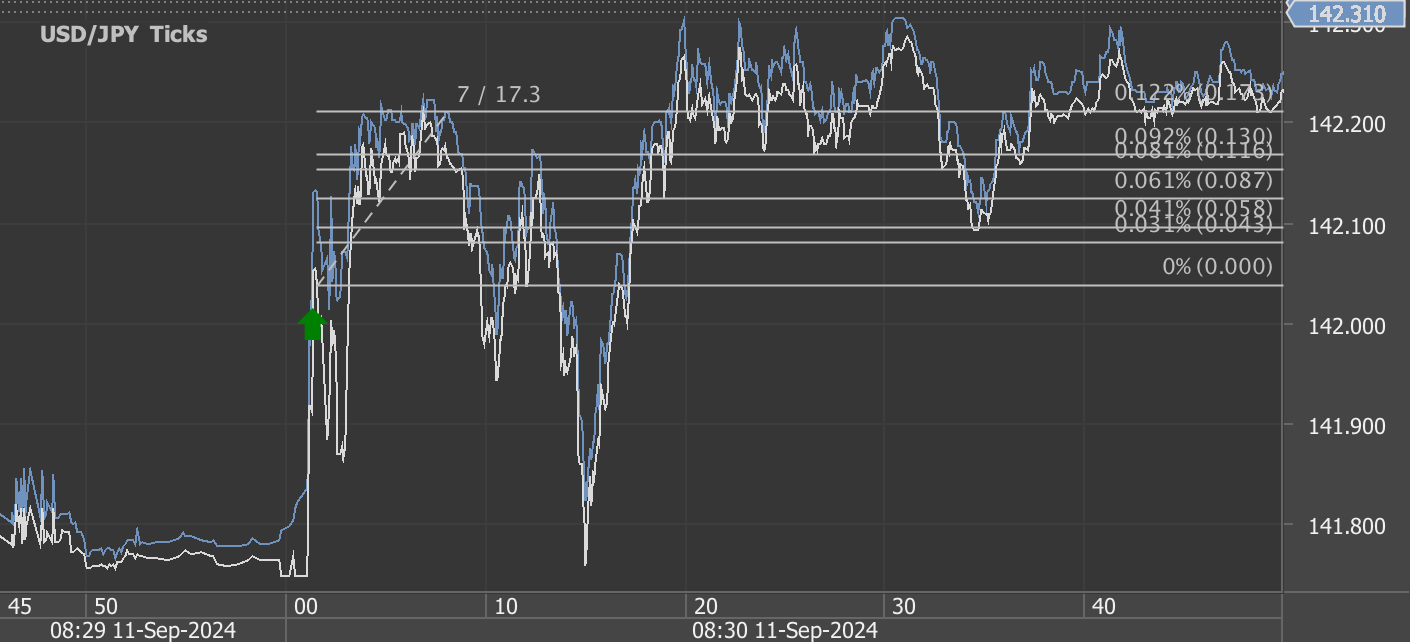

According to our analysis USDJPY and EURUSD moved 47 pips on US Retail Sales, US Jobless Claims and US Philadelphia Federal Reserve Bank Manufacturing Business Outlook Survey data on 17 October 2024.

USDJPY (32 pips)

EURUSD (15 pips)

Charts are exported from JForex (Dukascopy).

Economic Insights: Retail Sales, Unemployment Claims, and Manufacturing Outlook – October 17, 2024

Today, three significant economic reports were released, shedding light on the current state of U.S. retail, labor, and manufacturing sectors. These reports provide a snapshot of key economic indicators—retail sales performance, unemployment insurance claims, and regional manufacturing activity. Let’s break down each release to understand their implications and what they mean for the broader U.S. economy.

1. U.S. Retail and Food Services Sales - September 2024

The U.S. retail and food services sector continues to exhibit moderate growth, with September 2024 sales reaching $714.4 billion. This reflects a 0.4% increase from August 2024, and a 1.7% increase compared to September 2023. Over the three-month period from July to September, total sales grew 2.3% year-over-year, indicating a steady consumer demand despite economic headwinds.

Key highlights:

Nonstore retailers (e.g., e-commerce) showed remarkable resilience, posting a 7.1% year-over-year growth.

Food services and drinking places also saw an uptick, growing 3.7% from September 2023.

Traditional retail trade sales rose by 0.3% month-over-month and 1.4% year-over-year.

While the growth was moderate, the steady increase reflects resilience in consumer spending, a critical driver of economic activity in the U.S. economy. It will be important to monitor holiday season sales, as they could further influence retail performance into the year’s end.

2. Unemployment Insurance Weekly Claims - October 12, 2024

The labor market remains a focal point of economic analysis, and today’s unemployment insurance claims report offers some encouraging news. Initial jobless claims for the week ending October 12 decreased by 19,000 to 241,000, suggesting a stabilization in labor market conditions. While this is a positive sign, the four-week moving average—considered a more reliable indicator—rose slightly to 236,250, indicating some lingering volatility.

Other key labor data:

The insured unemployment rate remained steady at 1.2% for the week ending October 5.

Continuing claims (insured unemployment) rose by 9,000 to 1.867 million, signaling a slight increase in the number of individuals staying on unemployment benefits.

Despite this, the overall trend shows a labor market that remains robust, albeit with some fluctuations.

This drop in new claims aligns with the broader narrative of a tight labor market where employers are still holding on to workers despite broader economic uncertainty. However, as the Federal Reserve continues its balancing act between inflation control and employment growth, it will be important to watch whether these positive trends continue into the final months of 2024.

3. Manufacturing Business Outlook Survey - October 2024

The October Manufacturing Business Outlook Survey reveals encouraging signs of expansion in the manufacturing sector, particularly in the Mid-Atlantic region. The index for general activity surged to 10.3, up from 1.7 in September, marking a second consecutive month of growth. After a brief decline last month, both the new orders index (14.2) and shipments index (7.4) returned to positive territory, signaling renewed demand.

However, some challenges remain:

The employment index declined into negative territory at -2.2, suggesting that while most firms are maintaining steady employment, a small share of manufacturers are reducing their workforce.

Price pressures continue to persist, though the index for prices paid (input costs) dropped to 29.7, indicating a slight easing of inflationary pressures.

Looking ahead, manufacturers expressed optimism about future growth. The diffusion index for future general activity jumped to 36.7, with 47% of firms expecting increased activity over the next six months. This optimism is also reflected in anticipated capital expenditures for 2025, with 52% of firms planning to increase investments, particularly in software, hardware, and noncomputer equipment.

What Does This Mean for the Economy?

The combination of rising retail sales, stable unemployment claims, and expanding manufacturing activity paints a cautiously optimistic picture of the U.S. economy. While the labor market is still showing some signs of fluctuation, the underlying trends in consumer spending and manufacturing indicate resilience in key sectors.

The retail sector continues to grow, albeit modestly, suggesting consumers are still driving the economy forward. Meanwhile, the manufacturing sector is showing renewed strength, particularly in demand for goods. Labor markets remain tight, but the slight increase in continuing unemployment claims suggests there may still be some room for concern.

As we head into the holiday season and the final quarter of 2024, these reports will serve as important benchmarks for policymakers and investors. Will consumer demand stay strong? Can manufacturers keep pace with rising orders? And will labor markets continue to hold up against potential economic headwinds? These are the questions to keep an eye on as we move into 2025.

Stay tuned for further updates as more data emerges and economic conditions evolve.

Sources: https://www.census.gov/retail/sales.html, https://www.dol.gov/ui/data.pdf, https://www.philadelphiafed.org/surveys-and-data/regional-economic-analysis/mbos-2024-10

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.

Start futures forex fx news trading with Haawks G4A low latency machine-readable data today, one of the fastest news data feeds for US macro-economic and commodity data.