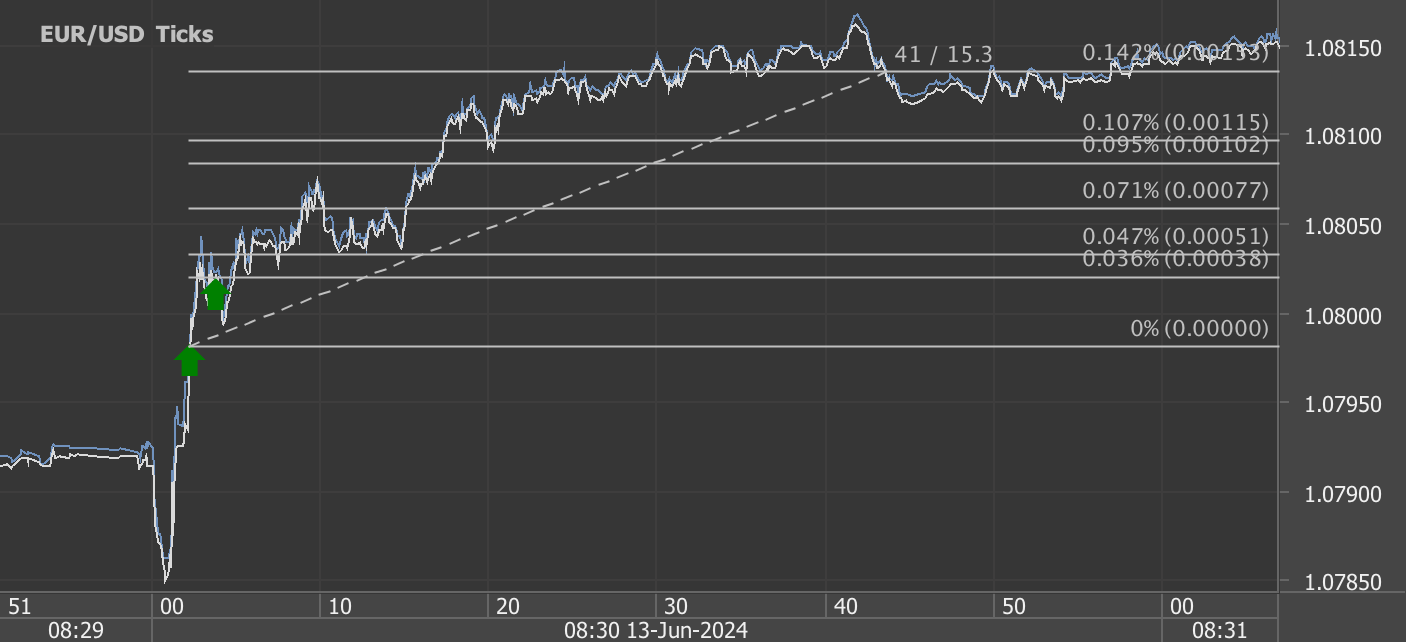

According to our analysis natural gas moved 40 ticks on DOE Natural Gas Storage Report data on 25 July 2024.

Natural gas (40 ticks)

Charts are exported from JForex (Dukascopy).

Understanding the Latest Trends in Natural Gas Storage

In the most recent Weekly Natural Gas Storage Report released on July 25, 2024, covering data up to the week ending July 19, 2024, we observe a detailed overview of the natural gas inventories across the United States. The Energy Information Administration (EIA) provides a comprehensive breakdown that not only informs stakeholders but also hints at broader economic implications.

Key Findings from the Report

Total Working Gas Increase: The total working gas in the underground storage was reported at 3,231 billion cubic feet (Bcf), marking an increase of 22 Bcf from the previous week. This suggests a slightly higher than expected accumulation, considering the week-on-week data.

Yearly and Historical Comparisons: When compared to the same period last year, current stocks are higher by 249 Bcf. Moreover, when measured against the five-year average from 2019 to 2023, stocks are up by 456 Bcf. These figures indicate a robust stockpiling activity that outpaces both last year’s figures and the longer-term average.

Regional Breakdown:

East: The East showed an increase to 697 Bcf, up from 686 Bcf the previous week.

Midwest: Stocks rose to 827 Bcf from 814 Bcf, showcasing a substantial net change.

Mountain: This region’s stocks saw a smaller increase, rising modestly from 248 Bcf to 251 Bcf.

Pacific: Remained steady at 289 Bcf, indicating stability in this region’s gas storage.

South Central: Interestingly, this region reported a slight decrease, down 6 Bcf from the previous week.

Coefficient of Variation and Standard Error: The coefficient of variation, an indicator of the variability relative to the mean of the dataset, remains low across the board, suggesting that the storage volumes are not prone to large swings, thus providing some stability in supply expectations.

Implications for Markets and Policy

The above-average stock levels relative to both last year and the five-year average can have several implications:

Market Impact: Higher storage levels typically moderate natural gas prices due to increased supply security. This could influence everything from residential heating costs to the operational costs for industries reliant on natural gas.

Policy Considerations: With an ongoing robust supply, policy makers might look at opportunities to adjust export levels or reconsider strategies for sustainable energy utilization.

Conclusion

As we head towards the latter part of 2024, the natural gas storage levels are demonstrating a significant cushion compared to historical levels. This robustness in natural gas storage not only helps in stabilizing prices but also plays a critical role in energy security during peak demand periods like winter. Going forward, stakeholders will be keenly watching the trends to gauge the potential economic and environmental impacts of these stock levels.

For more detailed insights and implications, stakeholders are encouraged to stay tuned for the next release on August 1, 2024, which will further shape the understanding of natural gas trends and strategic responses.

Source: https://ir.eia.gov/ngs/ngs.html

Start futures forex fx commodity news trading with Haawks G4A low latency machine-readable data, one of the fastest data feeds for DOE data.

Please let us know your feedback. If you are interested in timestamps, please send us an email to sales@haawks.com.